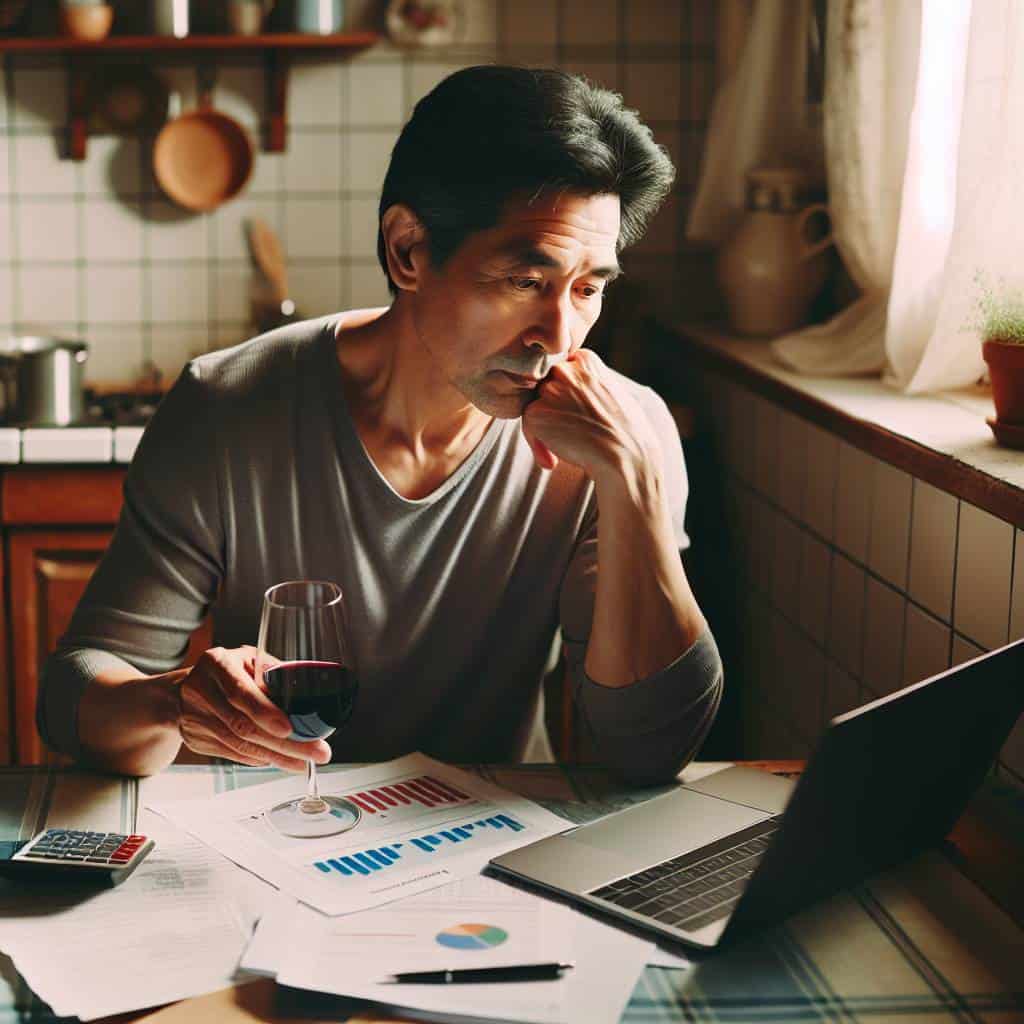

I remember the first time I sat down to figure out how much house I could afford. Armed with nothing but an online affordability calculator and a glass of cheap wine, I felt like a kid trying to assemble a jigsaw puzzle with missing pieces. The numbers danced around on the screen, mocking my naive optimism. I quickly realized that these calculators, with their neat little boxes for income and expenses, are about as useful as a chocolate teapot when you’re knee-deep in student loans. They don’t tell you about the unexpected costs—like the time I had to replace my entire heating system in the dead of winter.

So here’s what we’re going to do. We’ll cut through the digital noise and tackle the gritty details of home affordability. Forget the glossy brochures and the pie-in-the-sky loan estimates. We’ll talk about debt-to-income ratios, dissect the real impact of your credit score, and yes, we’ll even get into the nitty-gritty of budgeting for those hidden costs that no one likes to talk about. By the end, you’ll have a blueprint not just for a house, but for a home you can actually afford. Let’s dive in.

Table of Contents

Dancing on the Razor’s Edge: The Budget Tango with Affordability

The dance of budgeting for a home purchase is not for the faint-hearted. It’s a tango where each step must be calculated, every pivot precise; otherwise, you risk stepping over the razor’s edge into financial chaos. When you’re determining how much house you can afford, it’s not just about numbers on a page—it’s about understanding the rhythm of your financial life. The affordability calculators out there? They’re like dance partners that keep time but don’t lead. They’ll show you the framework, but the real choreography lies in your hands, or rather, in your debt-to-income ratio. This ratio, the unsung hero or villain of your financial story, tells you how your income stacks up against your debts. It’s the beat you must keep in mind as you navigate this complex dance.

But let’s get real. A budget isn’t just a set of limits. It’s a map to your future, with affordability as the compass guiding you through the tangled streets of mortgage rates, property taxes, and maintenance costs. Your budget is your lifeline, the whisper in your ear reminding you not to overstep. It’s easy to get swept away by the allure of hardwood floors and granite countertops, but the true art of this dance lies in balancing desire with reality. The goal isn’t just to afford a house; it’s to afford a life. One where your home doesn’t become an anchor dragging you down, but a foundation from which you can build the life you’ve envisioned. Remember, the dance floor is yours, and every step you take should lead you closer to a future that’s not just affordable, but sustainable.

The Cold Calculus of Home Buying

In the end, an affordability calculator is just a mirror reflecting your financial truths—no amount of wishful thinking will change your debt-to-income reality.

The Aftertaste of Reality

In the labyrinth of numbers and ratios, I’ve learned that true clarity doesn’t come from the sterile glow of a screen but from the gritty reality of my own financial landscape. It’s easy to get swept away by the allure of a dream house, seduced by square footage and premium finishes. But the real challenge is not drowning in the sea of mortgage options and interest rates. It’s about facing the cold, hard truth of my debt-to-income ratio and what it whispers about my financial future.

So, where does that leave me? With a newfound respect for the delicate dance between aspiration and pragmatism. Because, at the end of the day, owning a home isn’t just about what I can afford on paper. It’s about what I can sustain in my life. The calculators and ratios are mere stepping stones in this journey, not the destination. And that’s a reality I’m learning to embrace—one carefully calculated step at a time.